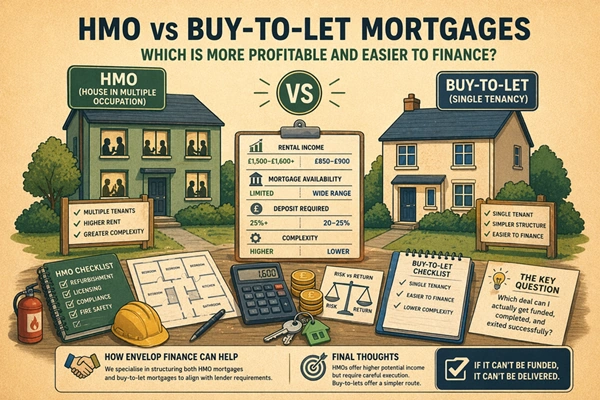

HMOs (Houses in Multiple Occupation) are typically more profitable due to higher rental income, but they are harder to finance and manage. In contrast, standard buy-to-let properties are easier to finance and more predictable, but generally offer lower yields.

When comparing an HMO mortgage vs a standard buy-to-let mortgage, most property investors focus on income potential, but profitability isn’t just about rent. Financing, costs, and long-term sustainability all play a crucial role.

In this guide, we break down the key differences between HMOs and buy-to-let properties, helping you choose the right strategy based on your goals, experience, and ability to secure funding.

| Factor | HMO | Buy-to-Let |

| Profitability | Higher gross rental income | Lower but more stable income |

| Net Yield | Can be higher, but reduced by costs | More predictable returns |

| Mortgage Approval | More difficult (specialist lenders) | Easier (wide lender choice) |

| Deposit Required | Typically 25%+ | Typically 20–25% |

| Interest Rates | Often higher | Usually lower |

| Management | Complex (multiple tenants) | Simple (single tenancy) |

| Regulation | Licensing + stricter compliance | Minimal regulation |

| Risk Level | Higher (voids, complexity) | Lower overall risk |

| Best For | Experienced investors | Beginners / hands-off investors |

What is the difference between an HMO and a buy-to-let?

Before comparing returns, it’s important to understand how these two property investment models work.

- Standard Buy-to-Let (BTL):

A single property rented to one tenant or household under one tenancy agreement. - HMO (House in Multiple Occupation):

A property rented out to multiple tenants individually, typically by room, with shared facilities.

These structural differences directly impact rental income, financing options, costs, and risk levels.

Rental income: Do HMOs really make more money?

One of the biggest advantages of HMOs is their higher gross rental yield.

Example comparison:

- Standard Buy-to-Let:

- Monthly rent: £850 – £900

- One tenant, stable income

- HMO Property:

- Monthly rent: £1,500–£1,600+

- Multiple tenants paying per room

This increase in rental income is why many investors are drawn to HMOs.

Key insight:

While HMOs typically generate higher gross income, this does not automatically mean higher net profit once costs, financing, and management are factored in.

Financing: Which is easier to get approved?

This is where the biggest difference lies, and where many investors underestimate the challenge.

Standard buy-to-let mortgages

- Wide range of lenders available

- Straightforward approval criteria

- Lower deposit requirements (typically 20–25%)

- Faster processing times

Result: Easier to finance, especially for new investors.

HMO mortgages

- Smaller pool of specialist lenders

- Stricter underwriting criteria

- Higher deposit requirements (often 25%+)

- More detailed rental stress testing

Lenders consider HMOs higher risk due to:

- Increased management complexity

- Higher tenant turnover

- Regulatory and licensing requirements

Result: More complex to finance, requiring careful deal structuring.

Real-world scenario: Two investment strategies

Let’s compare how this plays out in practice.

Investor A: Standard buy-to-let

- Property price: £180,000

- Monthly rent: £850

- Deposit: 25%

- Mortgage approval: straightforward

Outcome:

Smooth purchase process with multiple lender options and predictable timelines.

Investor B: HMO investment

- Property price: £180,000

- Expected rent: £1,600 (post-conversion)

- Additional costs: refurbishment, compliance, licensing

- Mortgage approval: more complex, limited lenders

Outcome:

Higher income potential, but longer timelines and tighter lending criteria.

Setup costs and on-going expenses

Buy-to-let

- Minimal upfront changes required

- Lower setup costs

- Predictable maintenance and management

HMO

- Conversion and refurbishment costs

- Fire safety and compliance upgrades

- Licensing fees (depending on local authority)

- Higher on-going management costs

Key Takeaway:

HMOs require more capital upfront and on-going involvement, which must be balanced against higher income.

Risk comparison: HMO vs buy-to-let

Buy-to-let risks

- Lower income ceiling

- Void periods if tenant leaves

- Slower portfolio growth

HMO risks

- Multiple room voids instead of a single tenancy

- Higher operational complexity

- Regulatory and licensing requirements

- Greater lender scrutiny

- Delays before generating income (conversion period)

Which strategy is right for you?

Choosing between an HMO and a buy-to-let property depends on your investment priorities.

Choose buy-to-let if you want:

- Simpler financing

- Lower upfront costs

- Predictable income and management

- Easier entry into property investing

Choose HMO if you want:

- Higher rental income potential

- Stronger yield opportunities

- Willingness to manage complexity

- Capacity to meet stricter lending criteria

HMO vs buy-to-let: Key decision factor

The real decision isn’t just about income, it’s about execution.

Many investors focus on projected rental returns but overlook:

- Whether the mortgage will be approved

- Whether the deal meets lender criteria

- Whether they can manage the property effectively

How Envelop Finance can help

Choosing between an HMO mortgage and a buy-to-let mortgage isn’t just about preference; it’s about what lenders will realistically support.

Envelop Finance works with property investors to:

- Match deals with suitable lenders

- Structure applications to meet lending criteria

- Reduce the risk of failed mortgage applications

- Identify viable investment strategies based on your profile

This approach helps investors move forward with confidence and clarity.

Common questions about HMO vs buy-to-let mortgages

Are HMOs more profitable than buy-to-let properties?

HMOs often generate higher rental income because multiple tenants pay rent per room. However, higher costs, such as licensing, maintenance, and management, mean net profit isn’t always significantly higher than a standard buy-to-let.

Is it harder to get an HMO mortgage?

Yes, HMO mortgages are typically harder to secure. Lenders apply stricter criteria, require larger deposits, and often expect landlords to have prior experience managing rental properties.

What deposit do you need for an HMO mortgage?

Most HMO mortgages require at least a 25% deposit, though some lenders may require more depending on the property type and borrower experience.

Are buy-to-let mortgages easier to get approved?

Yes, buy-to-let mortgages are generally easier to obtain. There are more lenders available, criteria are simpler, and the process is usually faster, making them more accessible for first-time investors.

Which is better for beginners: HMO or buy-to-let?

Buy-to-let is typically better for beginners due to simpler financing, lower upfront costs, and easier management. HMOs are better suited to more experienced investors who can handle complexity and higher risk.

Final thoughts: Yield vs simplicity

- HMOs offer higher income potential but require more effort, experience, and financing precision

- Buy-to-let properties offer a simpler, more accessible route with fewer barriers

The best strategy depends on your goals, experience level, and risk tolerance.

Focusing only on income can lead to costly mistakes. The most successful investors balance profitability with practicality, choosing deals they can actually execute and sustain long term.